11 Key Features to Compare Medicare Advantage Plans

Comparing Medicare Advantage plans without proper guidance can feel like putting together a puzzle with missing pieces. Your healthcare future depends on understanding what makes these plans different, whether you’re about to turn 65 or want to switch your current coverage.

Your typical Medicare Advantage plans offer services beyond original Medicare’s scope, such as dental, hearing, vision care, and prescription drugs . The projected average premium will reach $173 per month in 2025 , which makes choosing the right plan vital. Plus, plan structures differ by a lot—HMO plans need you to stick with in-network providers, while PPO plans let you see out-of-network doctors at higher costs .

The best time to pick your plan comes during the seven-month window around your 65th birthday (after getting Parts A and B) or during annual open enrollment from October 15 to December 7 . Note that $0 premium plans still require you to pay your Original Medicare Part B premium .

We’ve laid out 11 key features you should review while comparing Medicare Advantage plans. Our breakdown covers everything from enrollment periods to star ratings (Medicare reviews plans yearly on a 5-star system ) to guide you through your options confidently.

Enrollment Periods and Timing

Image Source: Insurance

You need to know the right time to enroll or switch Medicare Advantage plans to make better healthcare decisions. Each enrollment period has its own rules that affect your coverage choices.

What Enrollment Periods mean

Medicare Advantage enrollment periods let you join, switch, or drop your plan at specific times. Here are the six types of election periods:

Initial Enrollment Period (IEP): The 7-month window around your 65th birthday (3 months before, your birth month, and 3 months after) [1]

Annual Enrollment Period (AEP): From October 15 to December 7 each year [2]

Medicare Advantage Open Enrollment Period (MA OEP): January 1 to March 31 annually [2]

Special Enrollment Periods (SEPs): Available in specific situations like moving or losing other coverage [2]

Initial Coverage Election Period (ICEP): For those newly eligible for both Parts A and B [2]

Open Enrollment Period for Institutionalized Individuals (OEPI) [2]

How Enrollment Periods affect you

Each period gives you different options to change your coverage.

The Annual Enrollment Period lets you freely join, switch, or drop a Medicare Advantage Plan [2].

The Medicare Advantage Open Enrollment Period is more limited – you can only make one change if you’re already a member. You can switch to a different plan or go back to Original Medicare [3].

Your Initial Enrollment Period plays a vital role if you’re new to Medicare. Your coverage usually starts on the first day of your birthday month if you sign up in the first three months of your IEP [2].

You might qualify for a Special Enrollment Period if you miss these standard windows. This happens in special cases like moving away from your plan’s service area or joining a 5-star rated plan [2].

Local considerations for Enrollment Periods

Your location determines your enrollment options. States like Florida, Texas, California, and other areas where O’Neal Insurance operates have different plan options. Some states offer better choices than others.

Medicare Advantage plans work in specific service areas, so your address determines which plans you can join [2]. Moving to a new location usually qualifies you for a Special Enrollment Period to pick a new plan [2].

Cost impact of Enrollment Periods

Your enrollment timing can affect your wallet. Late enrollment penalties might increase your premium costs long-term if you miss your Initial Enrollment Period.

Switching plans during the Medicare Advantage Open Enrollment Period starts your coverage the next month [4].

This means starting over with a new deductible and out-of-pocket maximum [3].

Smart decisions during enrollment periods help you get the most from your benefits without extra costs. You should review your coverage options every Annual Enrollment Period. Plans often change their benefits and networks year to year, even if you like your current plan [1].

Monthly Premiums and Part B Costs

Image Source: ClearMatch Medicare

Monthly premiums play a key role when you compare Medicare Advantage plans. Original Medicare has standard costs, but these premiums change based on several factors, so you need to compare them carefully for your healthcare budget.

What Monthly Premiums mean

You pay Medicare Advantage premiums each month to keep your plan coverage, along with your required Part B premium [2]. Many people look at the Medicare Advantage premium alone, but you need to consider both costs:

Medicare Part B Premium: $185.00 per month in 2025 (standard amount) [1]

Medicare Advantage Plan Premium: Ranges from $0.00 to $200.00+ monthly [5]

The average Medicare Advantage premium for 2025 will be $17.00 monthly, a slight drop from $18.50 in 2024 [5]. About 60% of Medicare Advantage members won’t pay any premiums beyond their Part B costs in 2025 [5].

How Monthly Premiums affect you

While “$0 premium” plans might seem attractive, keep in mind that you’ll always pay your Part B premium no matter which Medicare Advantage plan you pick [5]. This required cost will affect your monthly budget.

Your income can change your costs too. People with high incomes pay extra monthly adjustments for Part B [1]. To cite an instance, if you earn above $106,000 (or couples above $212,000), you’ll pay higher premiums in 2025 [1].

The good news is that some Medicare Advantage plans give Part B premium rebates. Next year, 32% of plans will reduce the Part B premium—up from 19% in 2024 [2]. These rebates vary:

28% offer monthly reductions of $100.00+

25% offer reductions between $50.01-$100.00

17% offer reductions between $10.01-$50.00

30% offer reductions of $10.00 or less [2]

Local premium variations

Where you live changes your premium costs, which matters when you compare Medicare Advantage plans by state. States like Florida, Texas, and California show different premium averages because of market competition and healthcare costs.

O’Neal Insurance offers free consultations to help explain local premium differences in Florida, Texas, California, Mississippi, Nevada, and other states they serve.

Cost impact of Monthly Premiums

Medicare Advantage premiums have dropped from $36.00 in 2015 to $14.00 in 2024 [6], but the overall cost picture remains complex. Almost everyone (99%) can access at least one $0 premium plan [2].

All the same, don’t let premium cost alone guide your choice. Plans with higher premiums might save you money through better coverage or lower out-of-pocket costs. Even $0 premium plans could have higher deductibles or copayments.

Your premiums can change each year. Data shows that 83% of people who stay with Medicare Advantage will pay the same or less than they did in 2024 [2], which helps with budget planning.

Prescription Drug Coverage Options

Image Source: California Health Insurance

Prescription drug coverage is key when you compare Medicare Advantage plans. This is especially true since 90% of Medicare beneficiaries take at least one prescription drug regularly [5].

What Prescription Drug Coverage means

Medicare Advantage offers prescription drug benefits in two main ways. Most Medicare Advantage plans (MA-PDs) have drug coverage as part of their complete benefits package [7]. You can also add a separate Medicare drug plan (PDP) to Original Medicare [8]. Each plan uses a formulary—a list of covered medications in tiers that sets your cost-sharing [8].

Medicare Advantage plans with drug coverage must cover certain protected classes of medications. These include drugs that treat cancer, depression, HIV/AIDS, and other serious conditions [8]. Plan formularies also cover the most commonly prescribed drugs in various categories, though specific coverage differs between plans [8].

How it affects you

Your choice of drug plan determines which medications you can get and their cost. The 2025 guidelines state that enrollees pay a deductible of $590.00 (up from $545.00 in 2024). After that, you pay 25% of drug costs until you reach $2,000.00 in out-of-pocket spending [5]. Catastrophic coverage then kicks in with $0 additional costs [5].

Plans use several rules that control medication access:

Prior authorization requirements

Quantity limits

Step therapy (trying lower-cost alternatives first)

Pharmacy network restrictions [9]

Local plan differences

Drug coverage options vary by state. Medicare beneficiaries in 2025 will have access to about 15 stand-alone Part D plans and 34 MA-PDs in each region [5]. O’Neal Insurance serves states like Florida, Texas, California, Mississippi, Nevada, and others. Residents in these states should get customized advice about their local plan options.

Cost impact of drug coverage

Drug coverage can significantly affect your finances. The average Part D premium will drop by $7.45 in 2025, from $53.95 to $46.50 [10]. MA-PD plans usually cost less for drug coverage—just $13.50 on average in 2025 compared to $40.00 for stand-alone PDPs [10][5].

The Inflation Reduction Act brings changes in 2025. It caps yearly out-of-pocket prescription drug costs at $2,000.00 [5]. Most coverage stages will also limit insulin costs to $35.00 monthly per covered prescription [9].

Drug premiums are going down overall. However, you should check your specific medications when picking plans. Different formularies and tier placements can make a big difference in your total healthcare costs [5].

Provider Network Flexibility

Image Source: Paragon Health Institute

Provider networks are the foundations of how Medicare Advantage plans deliver care. These networks determine which doctors and facilities you can visit. Your choice of network affects both your access to care and what you pay out of pocket.

What Provider Network means

A provider network consists of healthcare providers—doctors, hospitals, and facilities—that partner with your Medicare Advantage plan to provide care [1]. Each plan type comes with its own network structure:

Health Maintenance Organizations (HMOs): You must use in-network providers except during emergencies. Your primary care doctor manages your specialist referrals [1].

Preferred Provider Organizations (PPOs): You can see specialists without referrals and use out-of-network providers at a higher cost [1].

Private Fee-For-Service (PFFS): These plans might have specific networks or “open networks” that let you see any provider who accepts the plan’s terms [6].

Medicare Advantage plans must follow network adequacy requirements set by CMS [1]. The networks need at least 27 types of provider specialties and 13 facility types within specific distances from where beneficiaries live [1].

How it affects your care

Your healthcare experience depends on your plan’s network structure. Many Medicare Advantage Plans tie your choice of primary care doctor to specific hospitals and specialty networks [6].

Provider networks help coordinate care better and reduce duplicate tests and services [1]. Research shows that poor coordination between providers results in conflicting information and higher rehospitalization rates [1].

Notwithstanding that, network limits can seriously affect your health. To cite an instance, Medicare Advantage members get complex cancer surgery less often at designated cancer centers or high-volume hospitals known for better outcomes [11].

Local provider access

Your location plays a big role when you compare Medicare Advantage plans by state. States served by O’Neal Insurance (Florida, Texas, California, Mississippi, and Nevada) offer different plan options and network sizes.

Plans can add or remove providers throughout the year [6]. Your provider might leave your plan’s network anytime. The plan should try to notify you at least 30 days before this happens [6].

Cost impact of network use

Out-of-network care costs more. HMO members who choose out-of-network providers must pay all costs themselves, except in emergencies. Neither the HMO plan nor Traditional Medicare covers these services [12].

Emergency services remain covered whatever the network status [13]. Current rules protect you from paying out-of-network cost-sharing for emergency care [1].

Networks help cut costs beyond direct expenses. They reduce duplicate and unnecessary costs, which make up about $130 billion of the $765 billion wasted in health spending each year [1].

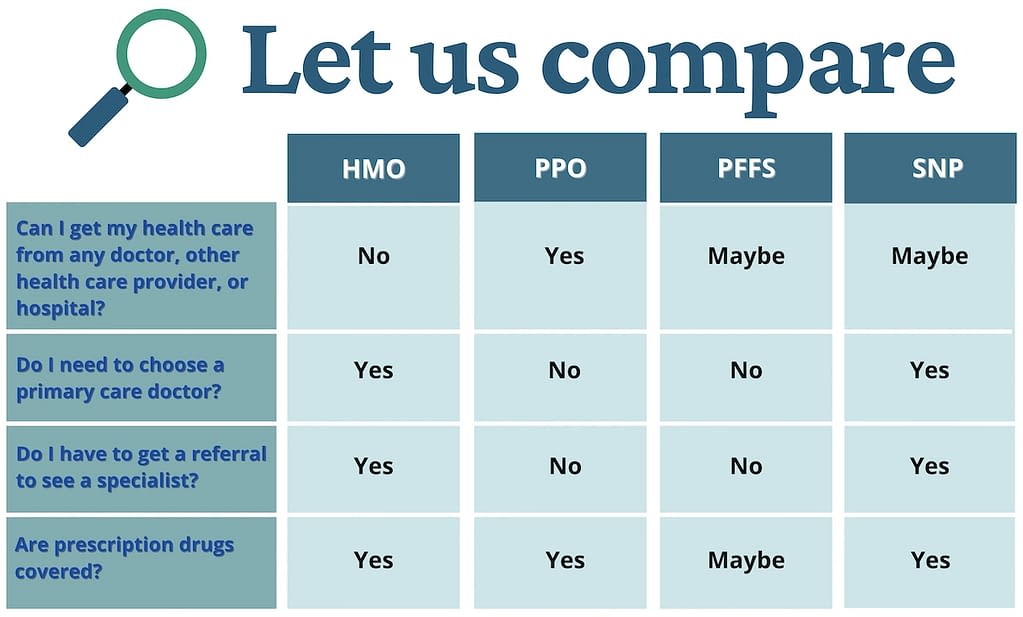

Referral Requirements for Specialists

Image Source: May River Medicare

Medicare Advantage plans have very different referral rules. These rules can make it easy or hard to see specialists. You should know these requirements to avoid unexpected costs and delays in your medical care.

What Referral Requirements mean

A referral works as a written order from your primary care physician to another healthcare professional. Your doctor gives background details and suggests what consultation or test you need medically [14]. Most insurance companies need your doctor’s approval before they cover specialist services.

Regular Medicare (Parts A and B) lets you see specialists without referrals, as long as the doctor takes Medicare assignment [14]. The rules are different for Medicare Advantage plans:

HMO plans: You need your primary care doctor’s referral to see specialists [15]

PPO plans: You can see specialists without referrals [2]

PFFS plans: You rarely need referrals for specialist care [2]

SNP plans: Referrals are usually needed, but some health screenings might not need one [2]

How they affect you

Referral rules decide how fast you can see a specialist. You’ll need to visit your primary care doctor first. They decide if you need specialist care [14].

The process has several steps. Your doctor talks about your condition and suggests specialists. They write up documentation and send it to both the specialist and your insurance company [14]. Remember – if you skip getting required referrals, you might have to pay the full specialist cost [2].

Local plan rules

Your location and specific plan affect referral policies. If you live in states where O’Neal Insurance operates (Florida, Texas, and California), check your local requirements. Even the same insurance company might have different rules for different plans.

Some HMO insurance companies only ask for referrals when you see specialists outside their network [2]. Plan rules can change each year. You’ll get a notice about changes in your Annual Notice of Change by September 30 [16].

Cost impact of referrals

Referrals can affect your wallet in several ways. Missing a required referral might leave you paying the full service cost [2]. You’ll also pay your share of the primary care visit just to get the referral [2].

Smart financial planning means checking referral requirements early. Factor in costs for both your primary care visit and specialist appointment.

Out-of-Pocket Maximums and Copays

Image Source: Boomer Benefits

You need to understand out-of-pocket maximums as a key protection when comparing Medicare Advantage plans. These protective caps put a limit on your yearly healthcare costs, and they change from plan to plan.

What Out-of-Pocket Maximums mean

The maximum out-of-pocket limit (MOOP) puts a yearly ceiling on your healthcare costs for Medicare Advantage Plans [8]. Your plan pays 100% of Medicare-approved Part A and B services after you hit this amount for the rest of the year [8]. Every Medicare Advantage plan must have this protection [17].

The federal maximum for in-network services is $9,350 in 2025 [8]. In spite of that, many plans set their limits lower, with $5,400 being the median out-of-pocket maximum [18].

These costs count toward your MOOP:

Deductibles

Copayments

Coinsurance

Your Part D prescription drug costs, premiums, and charges for non-covered services don’t add to this limit [8].

How they affect your budget

Medicare Advantage plans give you financial predictability, while Original Medicare has no out-of-pocket maximum [19]. This protection helps you especially when you have unexpected illness or injury that needs hospitalization [20].

PPO enrollees usually have two separate limits—one for in-network services and a higher limit that combines in-network and out-of-network care [8].

Your MOOP starts fresh each calendar year with new spending limits [21].

Local plan comparisons

MOOP amounts vary by region. James O’Neal Insurance gives free consultations to help residents in Florida, Texas, California, Mississippi, Nevada and other states understand their local options.

HMO enrollees have an average out-of-pocket limit of $3,965 [22]. PPO enrollees face higher limits – local PPOs average $8,634 while regional PPOs average $10,728 for combined in-network and out-of-network services [22].

Cost impact

MOOPs’ financial protection helps lower overall costs in Medicare Advantage. In fact, Medicare Advantage enrollees spend 18-24% less out-of-pocket than Traditional Medicare beneficiaries [7].

A typical enrollee in 2019 paid average monthly out-of-pocket costs of $440 in Medicare Advantage compared to $579 in Original Medicare [7]. This difference grows even more for people with poor health [7].

Out-of-pocket maximums are just one feature to think about, but they give you vital financial protection that Original Medicare doesn’t have. This makes them a key part of evaluating your Medicare Advantage options.

Plan Star Ratings and Quality Scores

Image Source: CarePlus Health Plans

Medicare’s Star Rating System helps you compare Medicare Advantage plans with objective data. Quality metrics give you a clearer picture beyond just looking at prices.

What Star Ratings mean

Star Ratings show how well plans perform in various quality categories, scored on a scale from 1 to 5 (with 5 being excellent and 1 being poor) [9]. Each year, CMS looks at Medicare Advantage plans using more than 40 different quality measures [9] that include:

Customer service responsiveness

Member satisfaction and complaints

Preventive care accessibility (screenings, tests, vaccines)

Chronic condition management

Drug safety and pricing accuracy

Appointment availability and care access

These detailed assessments look at everything from members getting needed care to plans managing health conditions effectively [9].

How they affect your decision

Star Ratings are a great way to get comparative data after you narrow down plan choices based on your needs [9]. Looking at 2025, about 40% of Medicare Advantage plans with prescription drug coverage earned 4 or more stars [23].

Higher-rated plans get financial rewards from Medicare that go directly into member benefits [9]. Plans rated 4 or 5 stars usually offer improved coverage for dental, vision, and hearing services—which could lower your healthcare costs [9].

Local plan ratings

Plan quality differs a lot by region. To name just one example, standard 5-star Medicare Advantage plans in 2025 are available in just 13 states plus Puerto Rico [24]. People living in states where O’Neal Insurance operates (including Florida, Texas, and California) can ask for free consultations to find the highest-rated local options.

Experience makes a difference—plans running for 10+ years in the Medicare Advantage program usually get higher ratings than newer ones [23].

Cost vs. quality

Premium cost matters, but quality metrics should weigh heavily in your decision. Non-profit organizations do better than for-profit plans—56% of non-profit MA-PDs got 4+ stars compared to just 36% of for-profit plans [25].

Before you join any plan, check its star rating on Medicare.gov’s plan finder tool by typing in your ZIP code [26]. This simple comparison ensures you pick a plan that gives you both good value and quality care.

Extra Benefits (Dental, Vision, Hearing)

Image Source: Senior Benefit Services, Inc.

Extra benefits serve as a major selling point to compare Medicare Advantage plans beyond standard Medicare coverage. These supplemental services help with crucial health needs that Original Medicare usually doesn’t cover.

What Extra Benefits mean

Medicare Advantage plans’ extra benefits include dental, vision, and hearing services that Original Medicare covers only in limited circumstances [16]. These supplemental benefits have become a standard feature in Medicare Advantage offerings:

99% of enrollees have access to vision coverage

98% have access to hearing benefits

96% have access to dental services [27]

Dental benefits usually cover preventive services like cleanings and exams. The detailed coverage (fillings, extractions, dentures) varies substantially between plans [28]. Vision benefits cover routine eye exams and allowances for eyeglasses. Hearing benefits include exams and sometimes hearing aid allowances [10].

How they affect your care

Studies show Medicare Advantage enrollees don’t typically use more supplemental services than those with traditional Medicare, despite having the coverage [5]. Many beneficiaries remain unaware of their benefits – only about 54% know they have dental or vision coverage [5].

Local availability

Most enrollees from major carriers can access these supplemental benefits, though coverage depth varies by region [27].

O’Neal Insurance offers free consultations to help residents in Florida, Texas, California, Mississippi, and other states understand their coverage options.

Cost impact

Medicare Advantage plans use rebate dollars to fund these extra benefits. The difference between the bid and standard reached nearly $2,000 per enrollee on average in 2022 [27]. Plans spent about $480 per enrollee on extra benefits from this amount [27].

Out-of-pocket costs still remain high. Medicare Advantage enrollees’ average payments were $226 for dental visits and $206 for eyeglasses – just 9% less than traditional Medicare users [5].

Plan Types: HMO vs PPO vs SNP

Image Source: Integrity Health & Life | Rochester, NY

Your Medicare Advantage plan’s structure shapes your healthcare experience completely. Understanding plan types reveals three main options that come with their own rules about care and costs.

What each Plan Type means

Health Maintenance Organization (HMO) plans work as coordinated care systems. These plans limit coverage to doctors and facilities within their network, except during emergencies [29]. You must pick a primary care physician to manage your care [1].

Preferred Provider Organization (PPO) plans give you more choices. Medicare-accepting doctors are available to you, though network providers cost less [29]. PPO plans don’t need a primary care physician or specialist referrals [1].

Special Needs Plans (SNPs) deliver targeted benefits to specific groups. These plans customize their benefits, provider choices, and drug formularies to match people’s needs who have certain diseases, healthcare requirements, or Medicaid eligibility [16]. Prescription drug coverage comes with all SNPs [29].

How they differ

The main differences between these plans include:

Network requirements: HMOs restrict you to network providers except during emergencies [30]. PPOs let you see out-of-network doctors at higher costs [6]. SNPs work like HMOs or PPOs based on the specific plan [16].

Primary care coordination: HMOs need a primary care doctor [29]. PPOs and many SNPs make this optional [1].

Specialist referrals: Your primary doctor must refer you in HMO plans [29]. PPOs skip the referral requirement [6]. SNP referral rules depend on their HMO or PPO structure [1].

Local availability

Your location determines which plans you can choose. Santa Clara County residents in California can access 22 HMO plans, 4 PPO plans, and 4 HMO-POS plans [12]. O’Neal Insurance helps you find local options through free consultations in Florida, Texas, California, and Mississippi.

Cost and flexibility

A clear balance exists between cost and flexibility. HMO plans usually keep premiums and out-of-pocket costs lower [30]. PPO plans cost more but let you choose providers freely [6]. SNPs focus on specialized care coordination and often provide care coordinators to help you access health services [16].

Local Plan Availability by State

Image Source: Gold Kidney Health Plan

Medicare Advantage plans are not equally available everywhere. Each state has its own mix of options, which makes finding the right coverage a challenge.

What Local Availability means

Your location plays a big role in which Medicare Advantage plans you can get. Insurance companies decide if they want to offer their plans across an entire state or just in specific counties [13]. Some plans work across state lines, but others only cover you in certain areas [31]. You might even find plans that limit how long you can stay outside your service area and still keep your coverage [31].

How to compare plans in your area

The average Medicare beneficiary can choose from about 42 Medicare Advantage plans in 2025 [31]. Looking at your options takes more than just checking premiums. You need to review provider networks, drug coverage, and extra benefits too.

O’Neal Insurance Group, a black-owned minority agency, helps people find the right plan at no cost. James O’Neal can meet with you by phone or Zoom to provide local agent support in Florida, Texas, California, Mississippi, Nevada, and many other states.

Where to compare Medicare Advantage plans

The Medicare.gov plan comparison tool is a great place to start [11]. Just enter your location and answer questions about financial assistance to see all plans that match your needs. This tool works best when you:

Enter your medications, dosages, and preferred pharmacy

Filter plans by benefits, type, ratings, carrier, and drug coverage

Select up to three plans to compare side by side

If you prefer talking to someone, State Health Insurance Assistance Programs (SHIPs) are a great way to get free guidance through shiphelp.org [11].

State-specific options

Plans are different between states and even between counties in the same state. Insurance companies might offer several plans in your area with different benefits and costs [13]. They can join or leave Medicare each year [13], which changes what’s available to you. Looking at resources specific to your state helps you find plans that match your exact location.

Using Medicare Plan Finder Tools

Image Source: AARP

Specialized comparison tools make finding the right Medicare Advantage plan easier. These digital tools help you find plans that match your healthcare needs, budget, and coverage priorities.

What Plan Finder Tools are

Medicare Plan Finder tools let you compare Medicare Advantage and prescription drug plans available in your area [32]. The Centers for Medicare & Medicaid Services (CMS) offers the most reliable option through their official Medicare.gov Plan Finder [33]. You can search for plans on this detailed platform by entering your zip code and answering a few simple questions about your coverage needs [32].

How to use them

The Medicare Plan Finder gives you two ways to access plan information:

Create an account/log in: Your information and medications stay saved for future visits [33]

Continue without logging in: You get immediate access without saving your data [33]

Pick your preferred method and follow these steps:

Enter your zip code and select your county [34]

Answer questions about your health, Medicaid status, and prescription needs [33]

Add your current medications to get accurate cost estimates [11]

Review available plans filtered by your priorities [33]

O’Neal Insurance Group, a black-owned minority agency, helps you navigate these tools at no cost. James O’Neal provides individual-specific guidance through phone or Zoom in several states including Florida, Texas, California, and Mississippi.

Best way to compare Medicare Advantage plans

The quickest way to compare plans involves:

Adding your specific medications, dosages, and preferred pharmacy to get precise cost estimates [11]

Using filters for benefits, plan types, ratings, and carriers [11]

Picking up to three plans to evaluate side by side [11]

Where to compare Medicare Advantage plans online

Insurance carrier websites and broker platforms complement Medicare.gov as helpful resources [35]. Double-checking details directly with plan providers will give a more accurate picture [35]. A licensed insurance agent can make this process smoother by discussing your healthcare needs and finding options that fit your situation [33].

Conclusion

You’ll need to think about several factors when picking the right Medicare Advantage plan. We’ve gotten into eleven key features that affect your healthcare experience and costs. Your personal healthcare needs should guide which elements matter most to you – from provider networks to prescription coverage, or extra perks like dental and vision care.

You don’t want to miss the specific time windows when you can make changes to Medicare Advantage plans. Mark these enrollment dates on your calendar right away. The cost picture goes beyond just premiums – you should know that the standard Part B premium will be $185.00 in 2025 whatever plan you pick.

Your coverage experience starts with choosing between different plan types. HMOs cost less but come with stricter networks, while PPOs give you more freedom at a higher price. Star ratings help you judge quality objectively. Only 40% of plans get 4 or more stars, though these top-rated plans usually offer better benefits.

The plans you can choose from depend on where you live. Medicare.gov‘s Plan Finder makes it easy to compare what’s available in your area. James O’Neal from O’Neal Insurance Group (a black-owned minority agency) can help you over phone or Zoom with free local agent support in Finding the Right original Medicare health insurance coverage and What to Expect During Your First Meeting with James O’Neal agent broker in:

Mobile Birmingham Alabama, Phoenix, Scottsdale, Mesa, Tempe, Chandler, Glendale, and Gilbert Arizona, Little Rock Arkansas, Oakland, Los Angeles, San Diego, California, Tampa Jacksonville Daytona Beach Pensacola Fort Lauderdale Miami Tallahassee Florida, Atlanta, Sandy Springs–Roswell, Augusta, Savannah, Columbus, Macon, Athens, Gainesville, Warner Robins, Valdosta, Dalton, Albany, Brunswick, Rome, and Hinesville Georgia, Oak Park Naperville Schaumburg Skokie Oaklawn Evergreen Park Joliet Kankakee Hyde Park Bolingbrook Chicago Illinois, Indianapolis, Fort Wayne, Evansville, Fishers, South Bend, Carmel, Bloomington, Hammond, Noblesville, Lafayette, Gary, Muncie, Schererville, Michigan City, Valparaiso, Crown Point, Merrillville, Danville, Chesterton, Griffith, Schererville, Indiana, Kansas Kentucky, New Orleans Louisiana, Henderson, Summerlin, North Las Vegas, Michigan, Jackson Hattiesburg Petal Gulfport Laurel Gulfport Biloxi Pascagoula Ocean Springs Moss Point Mississippi, Minnesota, Missouri, Montana, Nevada, New Mexico, New York, North Carolina, Ohio, Oregon, Pennsylvania, South Carolina, Tennessee, Houston, San Antonio, Dallas, Austin, Fort Worth, El Paso, Arlington, Corpus Christi, Plano, Lubbock, Laredo, Irving, Garland, Frisco, McKinney, Amarillo, Grand Prairie, Brownsville, Killeen, Denton, Texas, Utah, Virginia, Washington, D.C., District of Columbia, and Wisconsin.

Original Medicare doesn’t have maximum out-of-pocket limits, but these limits are vital protection against huge healthcare costs in Medicare Advantage plans. This protection becomes extra valuable when unexpected health issues come up. Your prescription drug coverage needs close attention since medications often make up much of healthcare costs. The 2025 changes will bring a $2,000 yearly cap on out-of-pocket prescription costs.

Time spent assessing these features helps you find coverage that fits your healthcare needs and budget. Medicare Advantage plans offer many benefits beyond Original Medicare. Look past the marketing hype to understand how each plan works for your specific situation.

Key Takeaways

When comparing Medicare Advantage plans, focus on these critical factors that directly impact your healthcare access and costs:

• Timing matters: Enroll during specific periods (Initial, Annual Oct 15-Dec 7, or Special) to avoid penalties and ensure coverage starts when needed.

• Look beyond $0 premiums: You’ll always pay the $185 Part B premium in 2025, plus potential plan premiums, deductibles, and out-of-pocket costs.

• Network flexibility affects access: HMO plans require in-network providers and referrals but cost less; PPO plans allow out-of-network care at higher costs.

• Out-of-pocket maximums provide crucial protection: Unlike Original Medicare, MA plans cap annual costs (federal max $9,350 in 2025), protecting against catastrophic expenses.

• Star ratings indicate quality: Only 40% of plans earn 4+ stars, but higher-rated plans often provide enhanced benefits and better care coordination.

• Use Medicare.gov Plan Finder: Enter your medications and zip code for accurate cost comparisons, or consult licensed agents for personalized guidance in your area.

The 2025 changes bring significant improvements, including a $2,000 prescription drug spending cap and continued access to extra benefits like dental, vision, and hearing coverage that Original Medicare doesn’t provide.

FAQs

Q1. What are the key differences between HMO and PPO Medicare Advantage plans? HMO plans typically have lower premiums but require you to use in-network providers and get referrals for specialists. PPO plans offer more flexibility to see out-of-network providers without referrals, but usually have higher costs.

Q2. How do Medicare Advantage plan star ratings impact my coverage? Star ratings (1-5 stars) indicate a plan’s quality and performance. Higher-rated plans (4+ stars) often offer enhanced benefits and better care coordination. However, only about 40% of plans achieve 4 or more stars.

Q3. What is the out-of-pocket maximum for Medicare Advantage plans in 2025? The federal maximum out-of-pocket limit for in-network services is $9,350 in 2025. However, many plans set lower limits, with the median being $5,400. This cap provides financial protection against catastrophic healthcare costs.

Q4. How does prescription drug coverage work in Medicare Advantage plans? Most Medicare Advantage plans include prescription drug coverage (MA-PD plans). In 2025, there’s a $590 deductible and a new $2,000 yearly cap on out-of-pocket prescription costs. Plans use formularies to determine drug coverage and costs.

Q5. When can I enroll in or switch Medicare Advantage plans? You can enroll during your Initial Enrollment Period (7 months around your 65th birthday), the Annual Enrollment Period (October 15 – December 7), or the Medicare Advantage Open Enrollment Period (January 1 – March 31). Special Enrollment Periods are also available in certain circumstances.

References

[1] – https://www.medicare.gov/publications/12181-3-6-24.pdf?linkit_matcher=1

[2] – https://www.medicare.org/articles/do-i-need-a-referral-to-see-a-specialist-with-medicare-advantage-plans/

[3] – https://www.medicareresources.org/medicare-eligibility-and-enrollment/the-medicare-advantage-open-enrollment-period-maoep/

[4] – https://www.ncoa.org/article/understanding-the-medicare-advantage-open-enrollment-period/

[5] – https://scitechdaily.com/medicare-advantage-exposed-higher-costs-same-benefits/

[6] – https://www.uhc.com/news-articles/medicare-articles/the-difference-between-medicare-hmo-and-ppo-plans

[7] – https://schaeffer.usc.edu/research/out-of-pocket-costs-are-substantially-lower-in-medicare-advantage-than-traditional-medicare/

[8] – https://www.medicareinteractive.org/understanding-medicare/health-coverage-options/medicare-advantage-plan-overview/maximum-out-of-pocket-limit

[9] – https://www.humana.com/medicare/medicare-resources/star-ratings

[10] – https://www.ncoa.org/article/what-medicare-covers-for-dental-vision-and-hearing-a-guide-for-older-adults/

[11] – https://www.nerdwallet.com/article/insurance/medicare/medicare-advantage-plans-how-to-compare

[12] – https://www.medicare.org/medicare-advantage-plans/california/santa-clara/

[13] – https://www.medicare.gov/health-drug-plans/health-plans/your-health-plan-options

[14] – https://www.healthline.com/health/medicare/does-medicare-require-referrals

[15] – https://www.ncoa.org/article/what-are-the-costs-of-medicare-advantage-part-c/

[16] – https://www.medicare.gov/publications/12026-understanding-medicare-advantage-plans.pdf

[17] – https://www.medicareinteractive.org/understanding-medicare/health-coverage-options/medicare-advantage-plan-overview/medicare-advantage-costs-and-coverage

[18] – https://bettermedicarealliance.org/news/new-analysis-shows-impact-of-recent-policymaking-on-medicare-advantage-plans-fewer-choices-higher-costs-and-reduced-benefits-for-seniors-in-2025/

[19] – https://www.medicare.gov/basics/costs/medicare-costs

[20] – https://www.humana.com/medicare/medicare-resources/medicare-out-of-pocket-cost

[21] – https://www.ncoa.org/article/what-you-will-pay-in-out-of-pocket-medicare-costs-in-2025/

[22] – https://www.kff.org/medicare/issue-brief/medicare-advantage-in-2024-premiums-out-of-pocket-limits-supplemental-benefits-and-prior-authorization/

[23] – https://www.cms.gov/newsroom/fact-sheets/2025-medicare-advantage-and-part-d-star-ratings

[24] – https://www.nerdwallet.com/insurance/medicare/best-medicare-advantage-plans

[25] – https://www.cms.gov/newsroom/fact-sheets/2024-medicare-advantage-and-part-d-star-ratings

[26] – https://www.forbes.com/advisor/health-insurance/medicare/medicare-advantage-in-pennsylvania/

[27] – https://www.kff.org/medicare/issue-brief/extra-benefits-offered-by-medicare-advantage-firms-varies/

[28] – https://www.ehealthinsurance.com/medicare/parts/can-i-get-extra-benefits-with-medicare-advantage/

[29] – https://www.medicare.gov/health-drug-plans/health-plans/your-coverage-options/compare

[30] – https://intermountainhealthcare.org/blogs/affordability-versus-flexibility-comparing-medicare-hmo-and-ppo-plans

[31] – https://www.medicalnewstoday.com/articles/medicare-advantage-plans-by-state

[32] – https://www.medicare.gov/plan-compare/

[33] – https://www.medicareadvantage.com/enrollment/medicare-plan-finder

[34] – https://www.ehealthinsurance.com/medicare/

[35] – https://www.medicalnewstoday.com/articles/how-to-compare-medicare-advantage-plans